Forecasts

- Overall CPI m/m is expected to show a 0.2% increase. The range of estimates is from 0.1% to 0.3%. Although the majority of economists surveyed by Bloomberg are aligned at 0.2%, there are a considerable amount predicting both 0.1% and 0.3%. I'd expect volatility regardless of any deviation.

- Core CPI m/m is expected between 0.4% and 0.5%. Some economists are calling for 0.3%. The average forecasts is 0.43%. Outside of the few calling for the 0.3%, there's almost an even split between 0.4% and 0.5%, with slightly more predicting a 0.4% print tomorrow for core CPI.

- CPI y/y follows the overall CPI forecasts. There's a range between 8.0% to 8.2%. While most are sitting at 8.1% there's enough at both 8.0% and 8.2% to expect some volatility regardless of any deviations from forecasts.

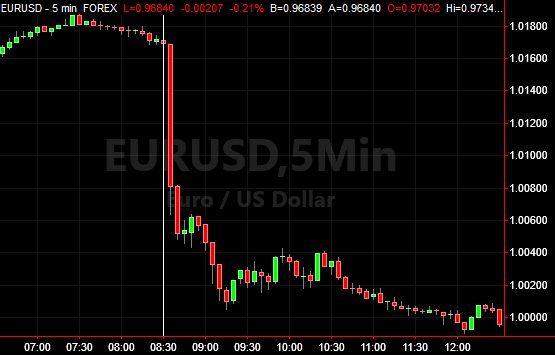

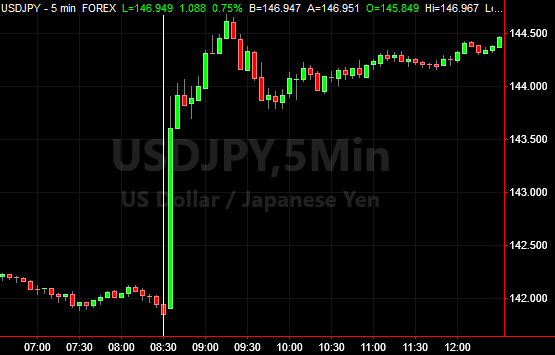

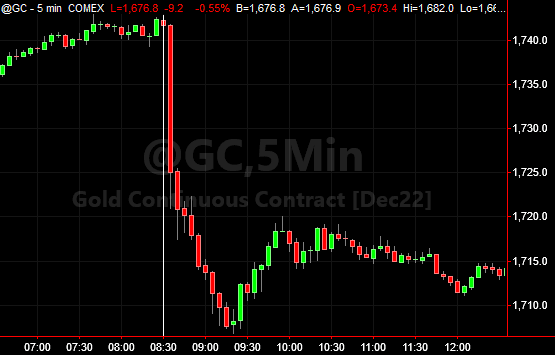

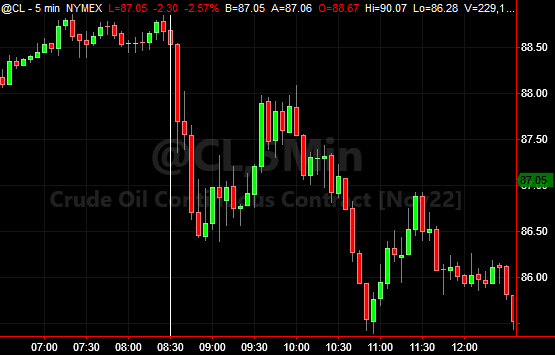

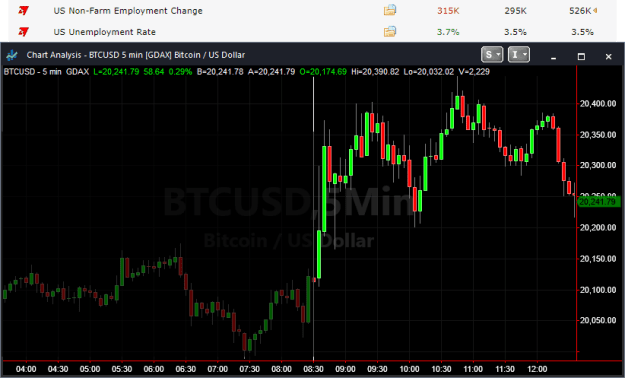

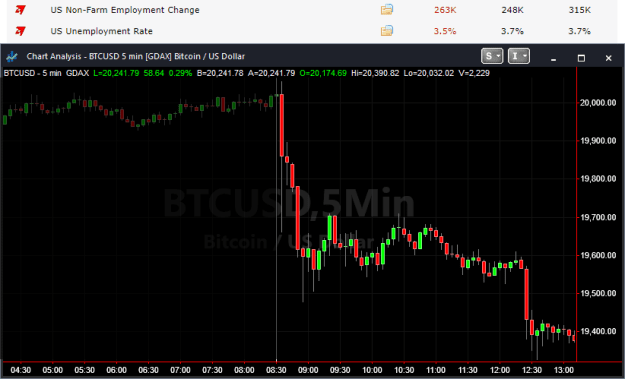

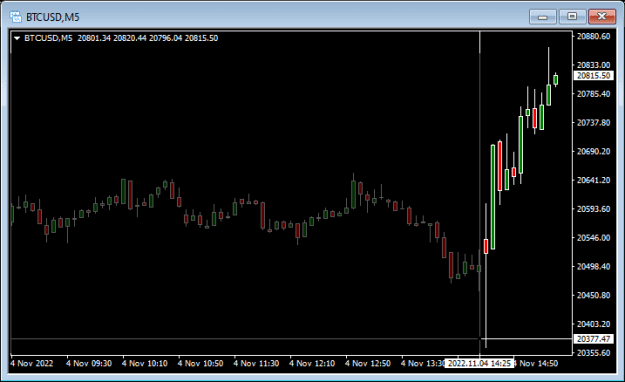

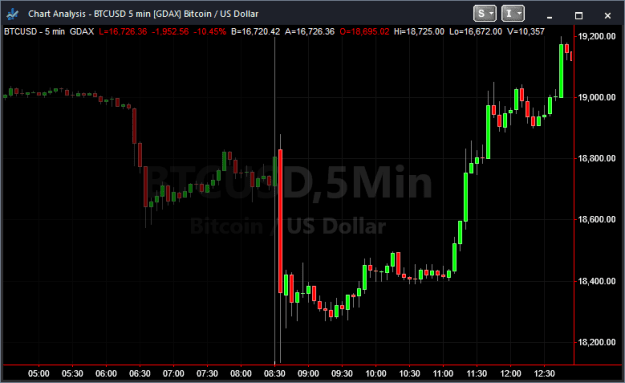

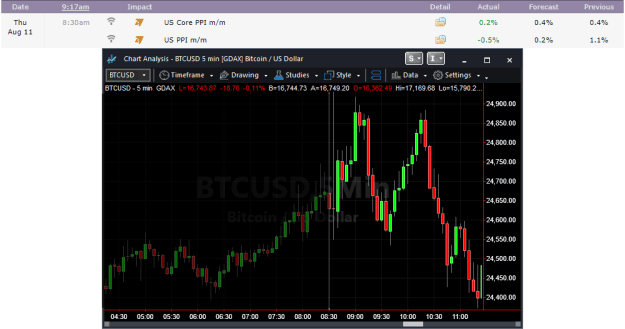

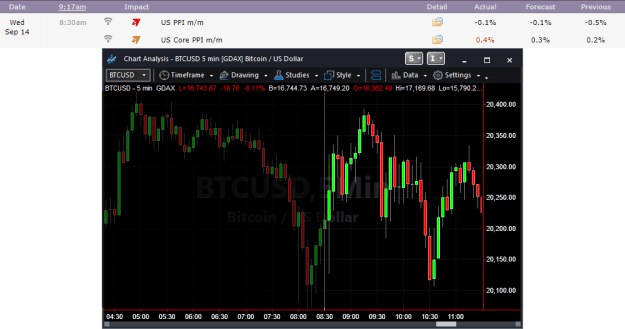

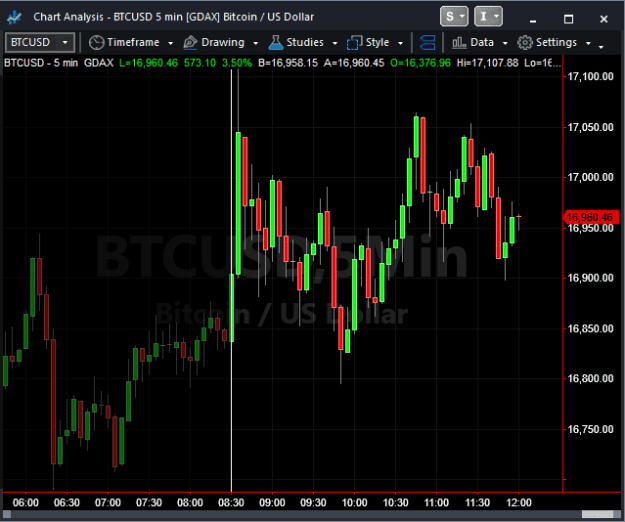

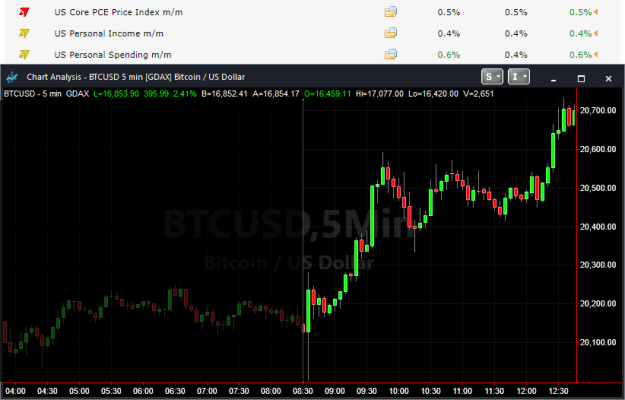

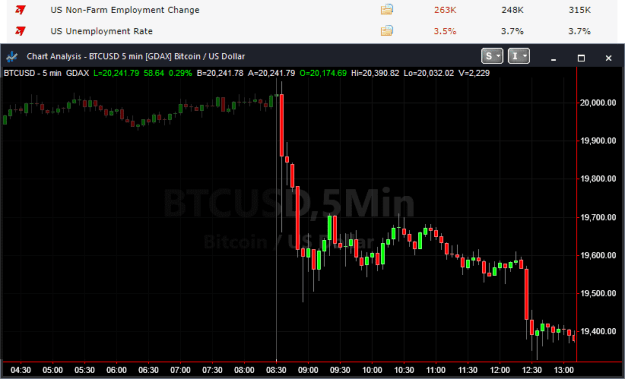

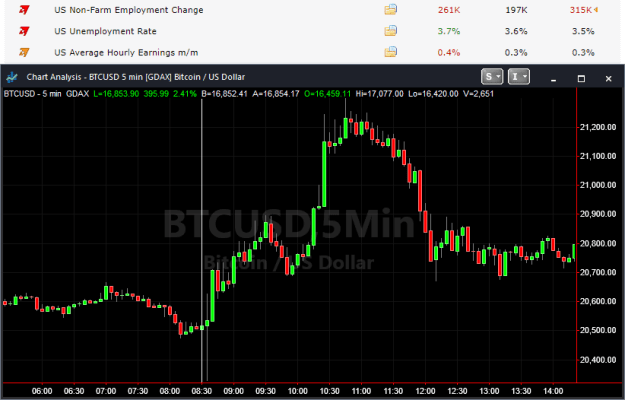

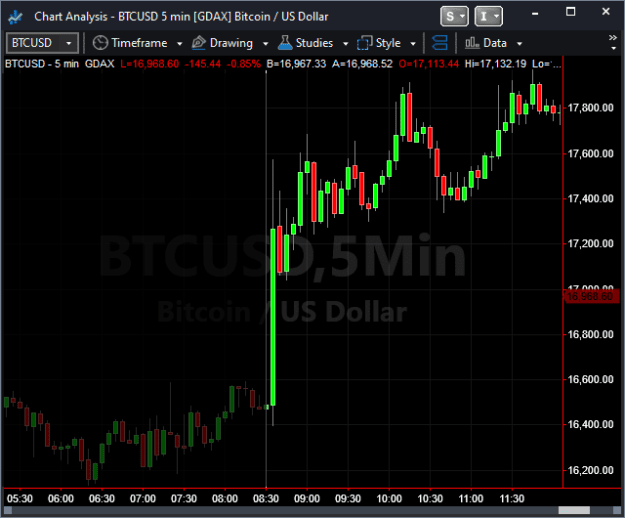

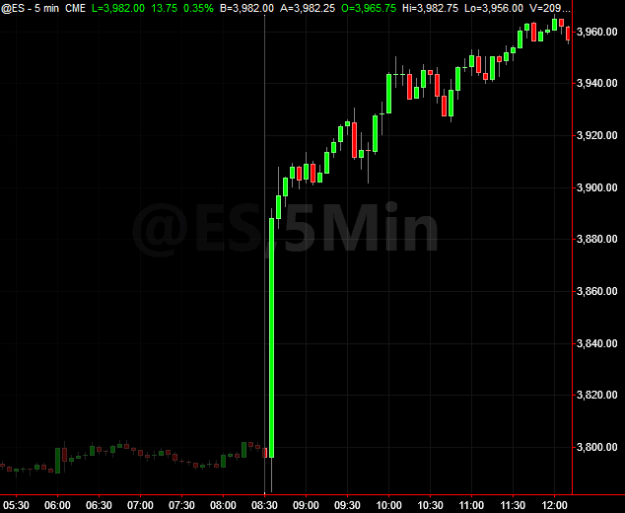

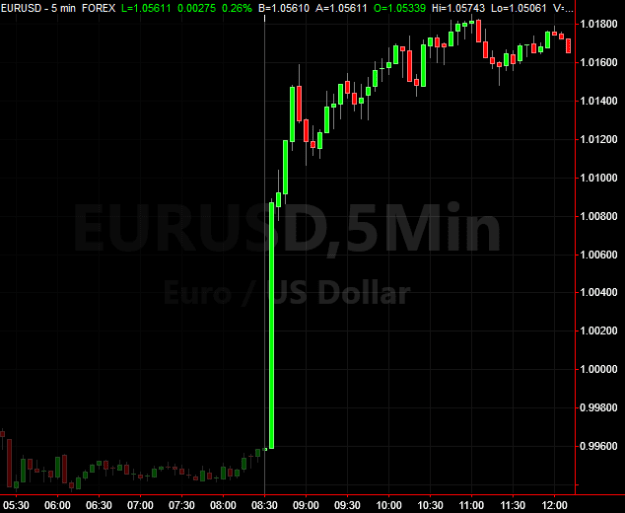

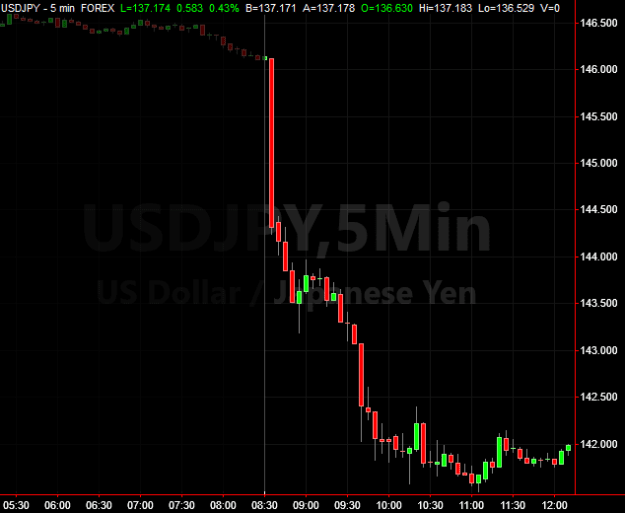

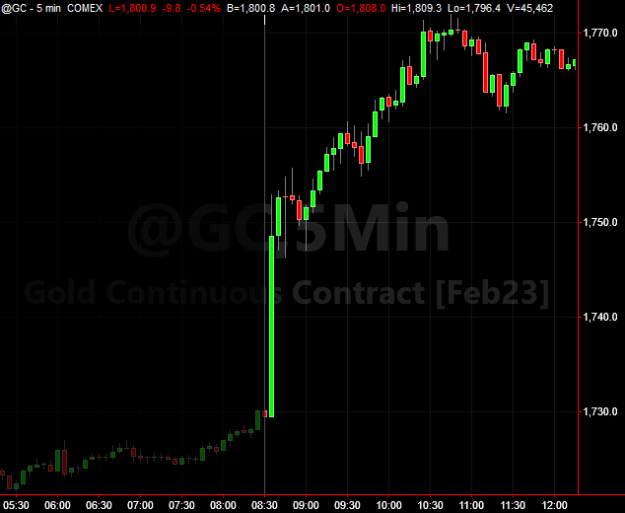

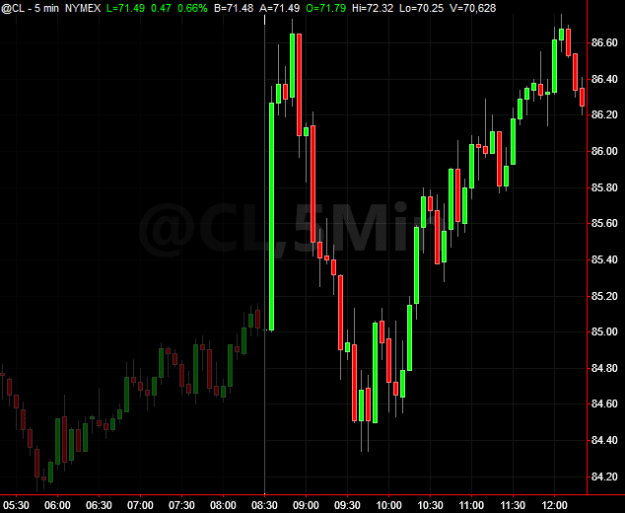

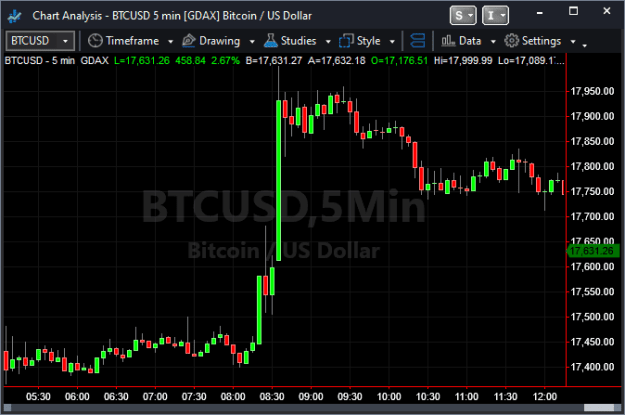

Recent impact (btc/usd) - See last month's US CPI data - September Follow up. This was the largest move on an economic data release (across asset classes) in recent memory.

Summary

As always, buckle up for US inflation data. US CPI data has been the most watched economic indicator for a while now. As the Fed wrestles with inflation, this data will tell us if the economy has responded to the Fed's aggressive rate hikes. So far, there's not much evidence it has.

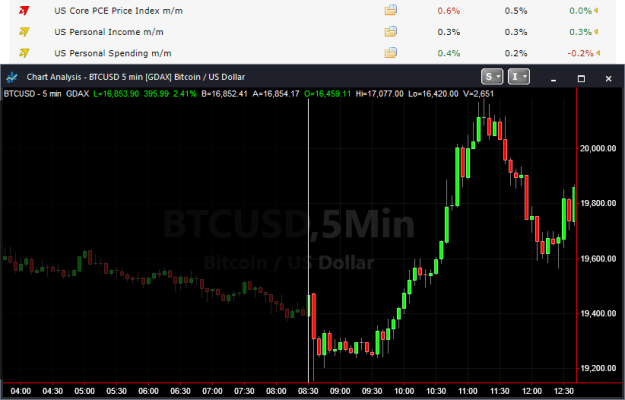

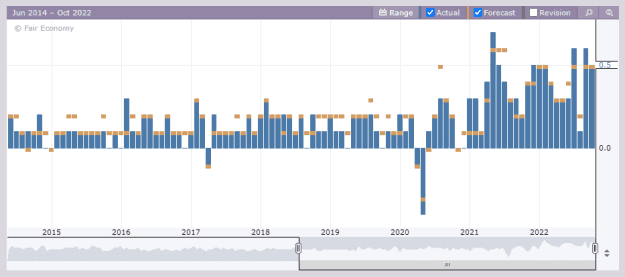

The most recent Core PCE Price Index print, the Fed's favored measure of inflation, came in higher than expected at 0.6% vs 0.5%, and 4.9% on an annual basis compared to a 4.7% prior. If CPI ticks up like PCE did, strap in.

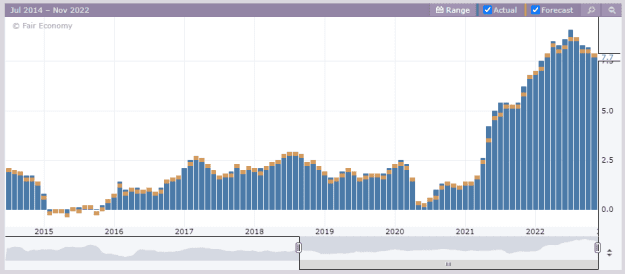

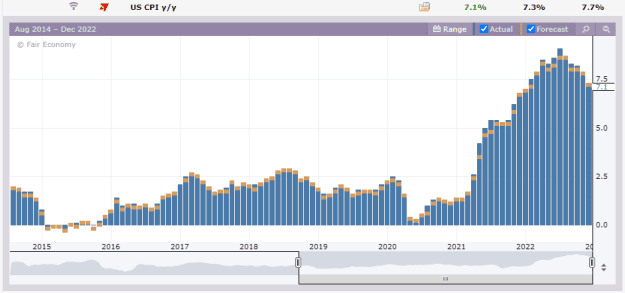

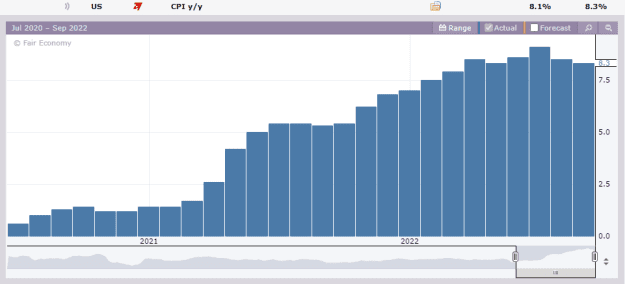

On a year over year basis, inflation started subsiding in July which was a measure as of June. That inflation figure was 9.1% followed by 8.5% in August and 8.3% in September.

Economists surveyed by Bloomberg are expecting this month's CPI data to show anywhere between 8.0% to 8.2% on an annual basis. Anything outside of that, I'd be expecting big moves with follow through. Although this scenario would require the core CPI data not being contradictory.

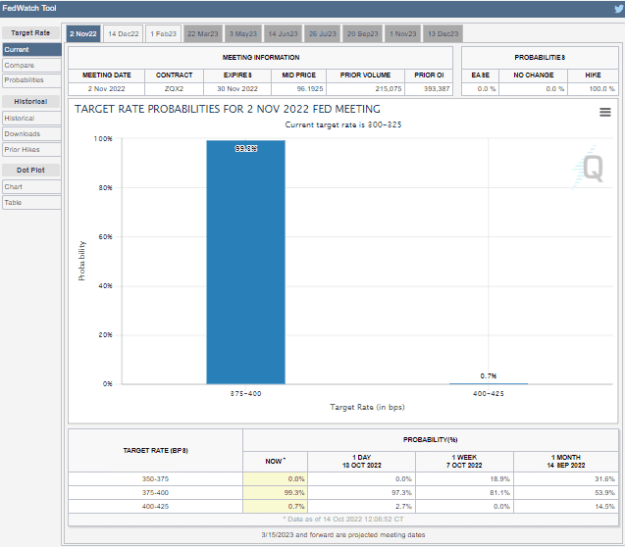

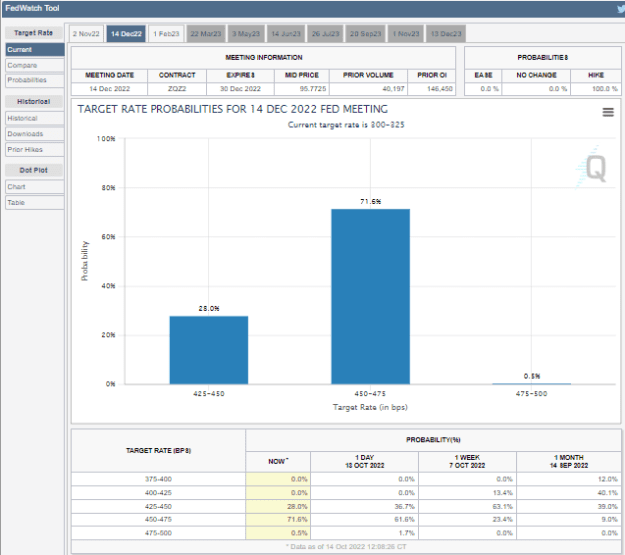

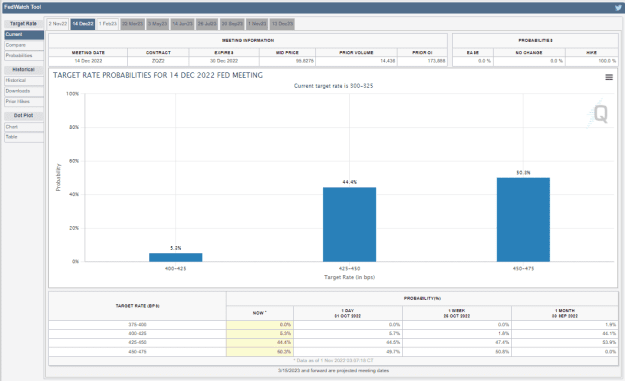

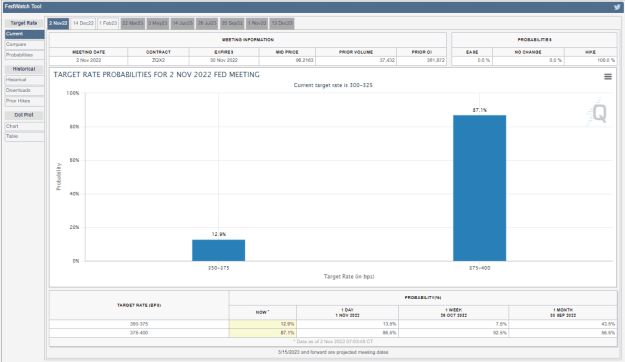

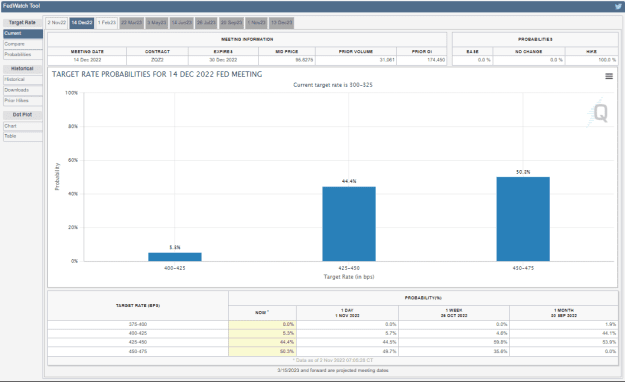

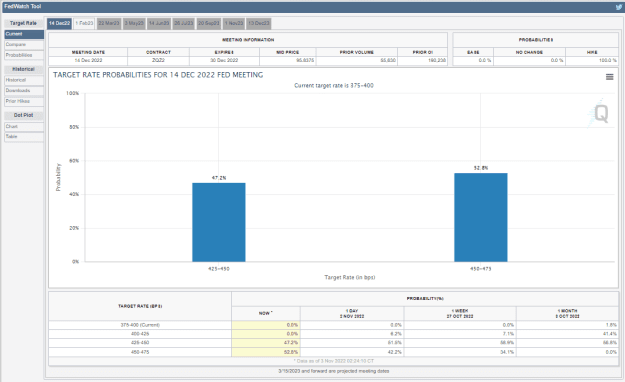

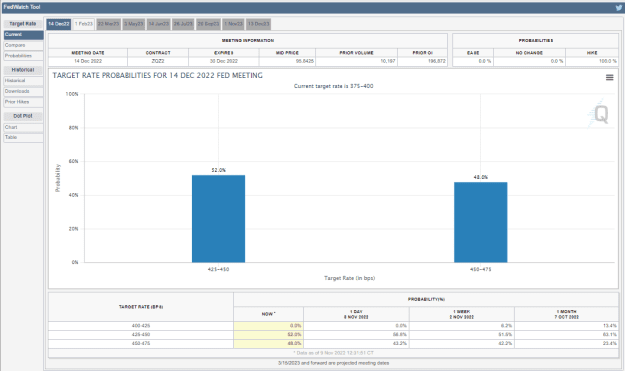

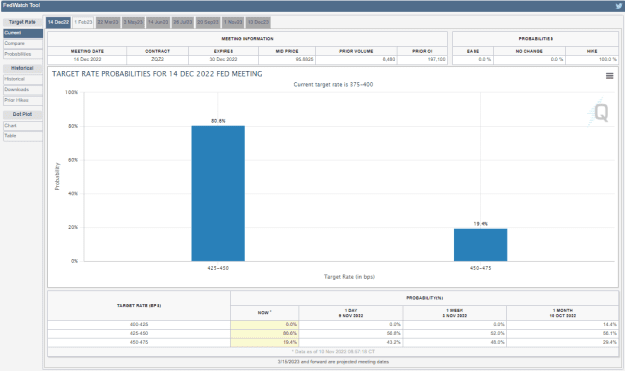

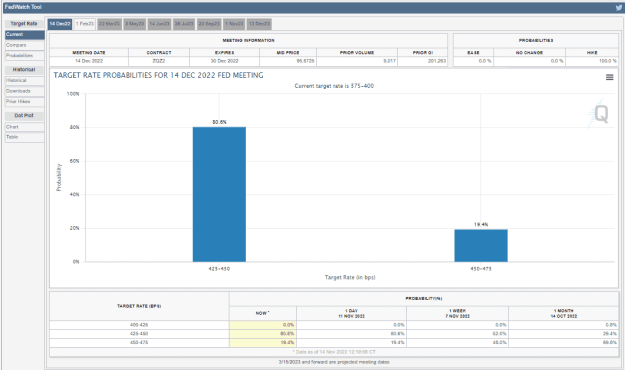

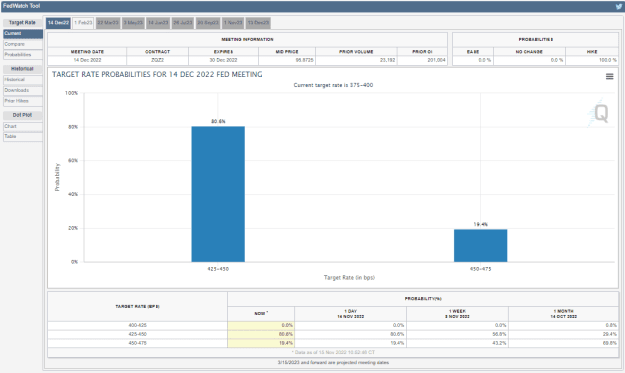

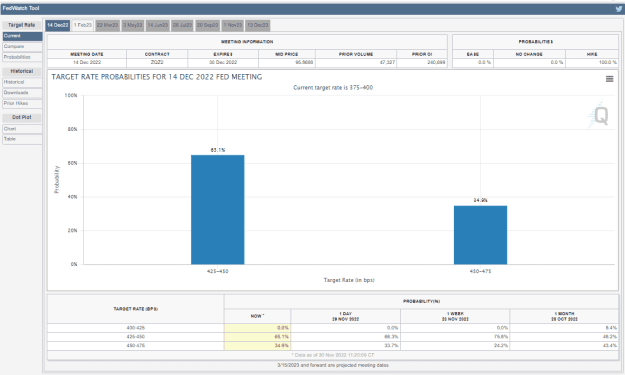

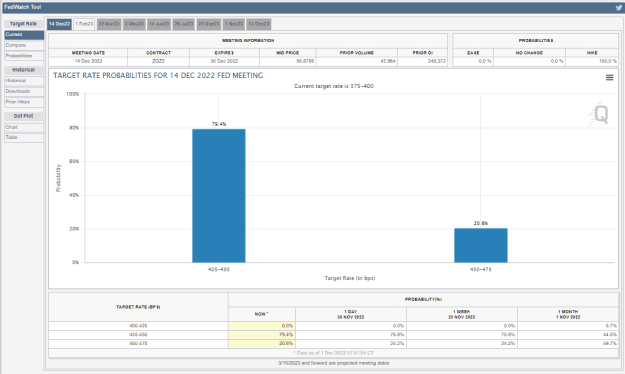

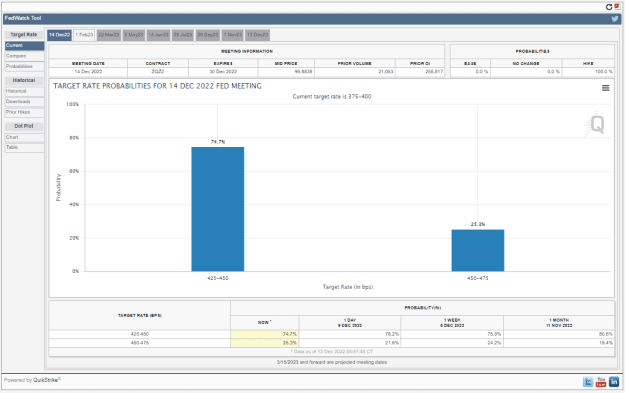

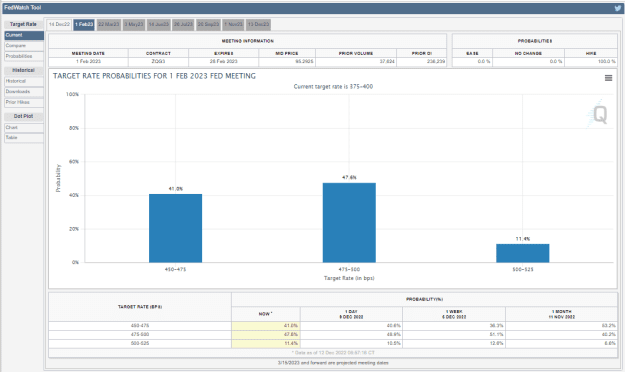

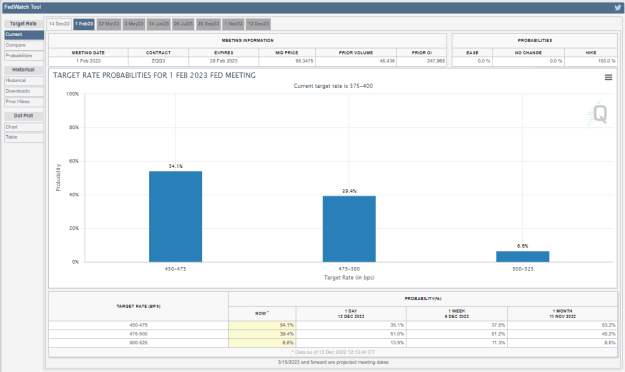

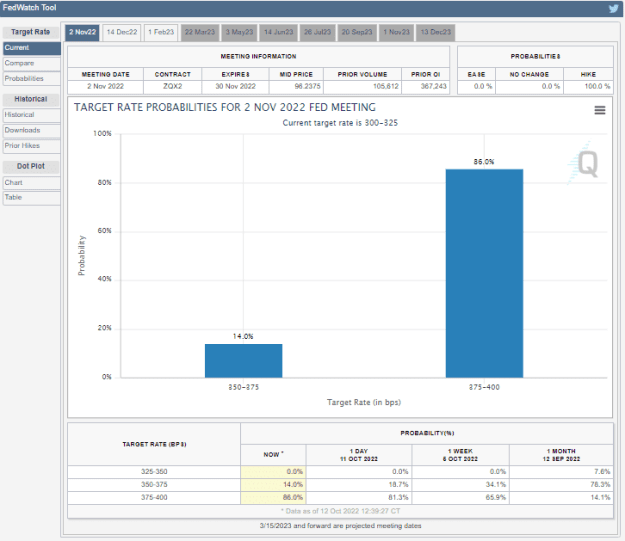

Currently, the markets are pricing in an 86% probability of a 75 bps rate hike in November. The December meeting is a lot more uncertain. It's mostly between a 50 and 75 bps hike. Rate probabilities:

November meeting:

December meeting:

On stronger than expected inflation data: Traders will start pricing in a greater chance of the 75 bps November rate hike. There's not much room to go from the 86% but expect that to go closer to being fully priced in (100%). Maybe more importantly, the December rate probabilities could see the markets start pricing in a greater chance of a 75 bps rate hike which would be significant considering only one Fed official predicted rates to reach 4.5% in 2022.

On weaker than expected inflation data: Barring any jarring miss, I wouldn't expect much movement in November rate probabilities. However, we could see a drastic decline in a 75 bps December hike probability as traders start pricing in a less hawkish post-November Fed. In this scenario the US dollar would fall while bitcoin appreciates.

It's important to always keep in mind with these releases where we see more than one data that they could contradict each other and result in a whipsaw. You don't want to be in the market when that happens.

I'd expect a lot of volatility at release time and we'll see a direction if both overall and core CPI both deviate from forecasts in the same direction.

As always, caution is advised.