-

FX Daily: Middle East turmoil strengthens US dollar position

It was reported overnight that Israel launched a retaliatory strike on the Iranian city of Isfahan. For now, it appears that Iranian media are downplaying the size of the attack, and reassured that nuclear facilities have not been affected. The news has had ramifications for different asset classes already, although the initial impact has partly been unwound in the early morning hours. After spiking above $90/bbl, Brent is trading at $89 at the time of writing, while the Nikkei dropped to as much as 3.5% but has now trimmed losses to 2.4%. Equity futures point to a -0.5/-1.0% open across US and European main stock ... (full story)

- Comments

- Subscribe

-

- Older Stories

From litefinance.org|Apr 19, 2024|1 comment

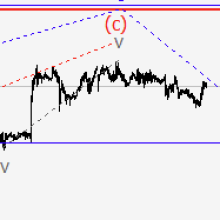

From litefinance.org|Apr 19, 2024|1 commentMain scenario: consider short positions from corrections below the level of 0.9235 with a target of 0.8325 – 0.8050. Alternative scenario: breakout and consolidation above the ...

From ecb.europa.eu|Apr 19, 2024

From ecb.europa.eu|Apr 19, 2024Since our last meeting in October, the global growth outlook has improved somewhat, reflecting revised growth prospects across both advanced and emerging market economies. The disinflationary process has continued amid falling energy prices, the normalisation of supply conditions and tight monetary policy. While the global economy has weathered the tightening of monetary policy well, growth prospects remain subpar by historical standards. Risks to the global outlook are broadly balanced for both economic activity and inflation, though rising geopolitical tensions pose an upside risk to inflation and a downside risk to growth. post: ECB'S PRESIDENT LAGARDE: THE DISINFLATION PROCESS IN THE EURO AREA HAS CONTINUED. post: ECB’s Lagarde: if Inflation Criteria Met, It Would Be Appropriate to Reduce the Current Level of MonPol Restriction ECB’s Lagarde: at the Same Time, the Governing Council is Not Pre-Committing to a Particular Rate Path post: ECB'S PRESIDENT LAGARDE: IF THE INFLATION CRITERIA IS MET, IT WOULD BE APPROPRIATE TO REDUCE THE CURRENT LEVEL OF MONETARY POLICY RESTRICTIONS.

From visualcapitalist.com|Apr 19, 2024|1 comment

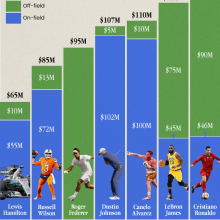

From visualcapitalist.com|Apr 19, 2024|1 commentHow much money do the world’s biggest athletes really make? And how do they compare across different sports? We visualized the highest earning athletes in various professional ...

-

- Newer Stories

From bankofengland.co.uk|Apr 19, 2024|1 comment

From bankofengland.co.uk|Apr 19, 2024|1 commentThank you to the Peterson Institute for the invitation to participate in today’s event focussing on the CEPR volume on monetary policy responses to the post-pandemic inflation1 . In line with the title of this panel I want to provide an update on my assessment of the evidence on what has caused the UK’s inflation2 . This evidence covers the key indicators of inflation and in particular persistence as well as associated analysis and what this implies for the extent to which the risks from persistence are receding. Economic forecasters have had a challenging time over the last few years in forecasting the inflation process, given the series of unprecedented and overlapping shocks which have hit the global economy. These challenges were highlighted in Ben Bernanke’s comprehensive review of the Bank’s approach to, and use of forecasting published last week. A key recommendation of the Bernanke review is that the Bank should make more systematic use of scenarios in framing the outlook for inflation and the implications for monetary policy, in a world characterised by greater uncertainty and significant structural changes. The Bank has committed to implementing all the recommendations of the review. As someone who has used scenarios throughout my career, I think this is the right direction for the Bank to go in. But we should travel with a high degree of humility, given the ongoing uncertainties a post: BOE'S RAMSDEN: THERE ARE LIKELY TO BE BUMPS IN THE DISINFLATION PROCESS FROM ONE MONTH TO THE NEXT. post: BOE'S RAMSDEN: THIS LEAVES THE UK AS LESS OF AN OUTLIER AND MORE OF A LAGGARD IN TERMS OF RECENT INFLATION PERFORMANCE. post: BOE'S RAMSDEN: INFLATION STAYING CLOSE TO THE 2% TARGET OVER THE WHOLE FORECAST PERIOD IS AT LEAST AS LIKELY AS THE FEBRUARY 2024 FORECAST. post: BANK OF ENGLAND MPC MEMBER DAVE RAMSDEN AT PETERSON INSTITUTE PANEL: I HAVE BECOME MORE CONFIDENT THAT THE RISKS OF PERSISTENT INFLATION ARE RECEDING #bankofengland #boe #daveramsden #monetarypolicy #interestrates #inflation #ukeconomy

From forexlive.com|Apr 19, 2024

From forexlive.com|Apr 19, 2024The IMF European regional report is out and says: • Soft landing for European economies is in reach but not assured - • High-debt European economies should consolidate fiscal ...

From chicagofed.org|Apr 19, 2024

From chicagofed.org|Apr 19, 2024video The U.S. economy made substantial progress in 2023 on the Federal Reserve’s dual mandate of maximizing employment and stabilizing prices. Inflation had one of the largest drops in the last 50 years and did so with solid growth, low unemployment, and no recession. So far in 2024, that progress on inflation has stalled. You never want to make too much of any one month’s data, especially inflation, which is a noisy series, but after three months of this, it can’t be dismissed. I am still hopeful that we will again see a return to improvement on inflation in the months ahead, as our restrictive monetary policy continues to curb inflation pressures and the economy continues returning to pre-pandemic norms. At the end of the day, we will get inflation back to target. I always say that the first rule for data dogs is that when you are uncertain, keep sniffing. Right now, it makes sense to wait and get more clarity before moving. We were at our 2 percent target before Covid, but not because inflation of everything was 2 percent.. Housing was around 3.5 percent, services 2.5 percent, and goods –1 percent. Much of the improvement in inflation last year came from positive supply developments. As the supply chains healed, goods inflation returned basically back to pre-Covid rates. Most of that supply healing is now complete. Part of the supply side benefit last year came from increases in labor supply, in part from immigration and in part from higher participation rates of many groups. The impact of that will likely continue to help the economy this year. While we saw deterioration in services inflation last month, there was surprising improvement over the course of 2023—it remains above pre-Covid trends, but there may be more space for progress. That leaves the main short-run problem as I see it, which is persistently high housing inflation—still much higher than it was pre-pandemic. Looking at market data on rents for new leases, I’d say housing inflation is supposed to have been falling. If it doesn’t, it will be hard to see a smooth path back to our 2 percent inflation goal. As we have seen strong gross domestic product (GDP) and jobs numbers, we need to determine if this is a sign of overheating driving up inflation. But let’s be careful: As I have said before, when there are supply side developments (for example, higher productivity growth, supply chain improvements, or increasing labor force participation or population growth), aggregate numbers are not great measures of overheating. There are crosscurrents at work. Not all the data s post: Goolsbee: Proper Fed Policy Going Forward Will Depend on the Data Goolsbee: Fed’s Current Restrictive MonPol ‘Appropriate’ Goolsbee: ‘Makes Sense to Wait’ to Get More Clarity Before Moving Fed’s Goolsbee Says Progress on US Inflation Has Stalled post: Goolsbee: Still Hopeful for Return to Improvement on Inflation in Months Ahead Goolsbee: Persistently High Housing Inflation’s Main Short-Run Problem Fed’s Goolsbee: We Have to Recalibrate, We Have to Wait and See post: ? GOOLSBEE: THE GOLDEN PATH IS MORE DIFFICULT FOR 2024 ? GOOLSBEE SAY REAL FED FUNDS RATE IS HISTORICALLY QUITE HIGH ? GOOLSBEE: THE POLICY TRADEOFFS ARE HARDER THIS YEAR post: Fed's Goolsbee: Unproductive Speculating On Conditions For Raising, Or Cutting, Rates - Determining Policy Restrictiveness Depends On The Data

- Story Stats

- Posted: Apr 19, 2024 10:00am

- Submitted by:Category: Fundamental AnalysisComments: 0 / Views: 2,423

- Linked event: