Prop Firm DrawDown Protector : Prop Firm Capital Protection Expert MT5 |Forex Money Management: Forex Trade Management Expert MT5 | ICT Concepts Indicator MT5 |Smart Money Concepts Expert MT5 | Smart Money Trap Scanner | Get a free Expert Advisor license via Telegram and WhatsApp

Why the Interest Rate is Important

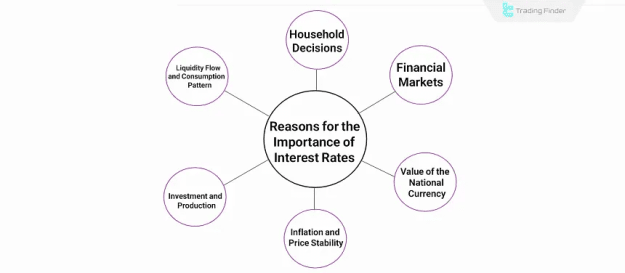

As the price of money, the Interest Rate is a core macroeconomic variable with widespread influence:

- Liquidity Flow and Consumption: Changes in the Interest Rate determine the direction of capital movement and significantly impact consumer behavior (saving vs. spending).

- Investment and Production: Lower Interest Rates reduce financing costs for businesses, thereby making new investments and production more attractive.

- Inflation and Price Stability: Higher Interest Rates are employed as a tool to reduce inflationary pressures and constrain credit growth within the economy.

- Impact on Currency Value: Interest Rate differentials with other nations directly influence the appeal of foreign investment and, consequently, affect exchange rates.

- Financial Markets: The level of Interest Rates is a key factor governing bond yields, the attractiveness of deposits, and the flow of capital into or out of stock markets.

- Household Decisions: Choices regarding current consumption versus savings are directly affected by the prevailing Interest Rate environment.

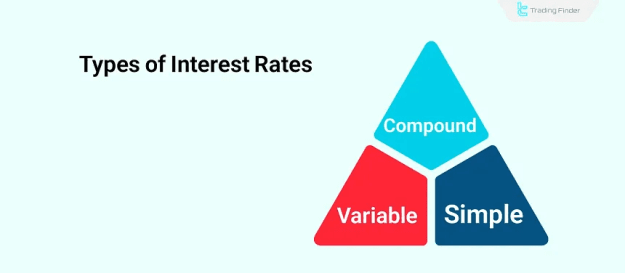

Types of Interest Rates

Interest Rates are categorized into simple, compound, and variable forms, which produce significant differences in repayment burdens or investment returns.

Simple Interest Rate

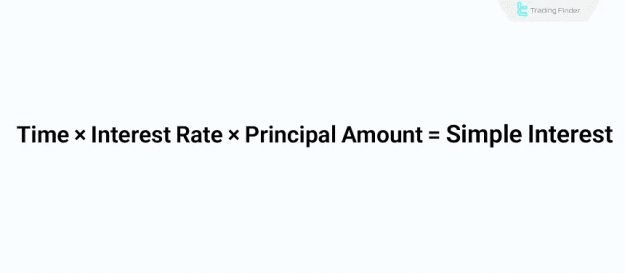

- Under Simple Interest, interest is calculated only on the principal amount in each period.

- There is no compounding effect; the interest earned does not accrue further interest.

- The simple interest calculation formula is:

$$\text{Simple Interest} = \text{Principal Amount} \times \text{Interest Rate} \times \text{Time}$$ - For example, a $\$1,000$ deposit at $10\%$ simple annual interest for three years yields $\$300$ in total interest.

Compound Interest Rate

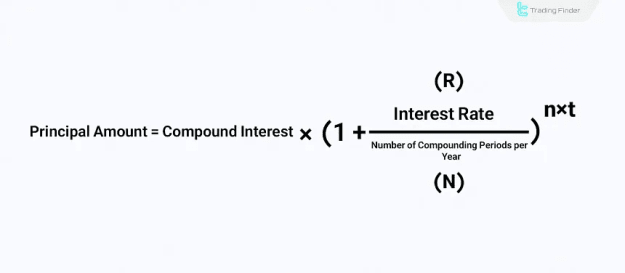

- With Compound Interest, the interest earned in each period is added to the principal for the subsequent period's calculation, resulting in the compounding effect.

- This approach generates significantly higher long-term returns compared to simple interest.

- The compound interest formula is:

$$\text{Future Value} = \text{Principal Amount} \times \left(1 + \frac{R}{N}\right)^{N \times t}$$

(where $R$ is the annual rate, $N$ is the number of compounding periods per year, and $t$ is the time in years). - For instance, a $\$1,000$ deposit for three years at $10\%$ compounded annually results in a future value of $\$1,331$.

Interbank Interest Rate

- The Interbank Rate is the short-term lending rate between banks in the repo market. It reflects banks' financing costs.

- An increase in the repo rate typically signals higher risk in the banking system.

Fixed and Variable (Floating) Rates

Borrowers can choose between these based on their expectations of future rate changes:

- Fixed Rate: Offers predictable installments and stability, shielding the borrower from rising rates.

- Variable (Floating) Rate: Provides the possibility of lower repayment costs if rates decline, but carries the risk of higher installments if rates increase.

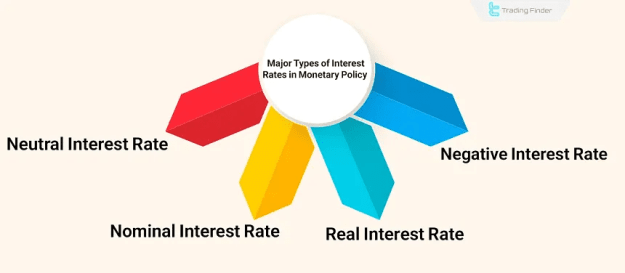

Application of the Interest Rate in Monetary Policy

The Interest Rate is the main tool for implementing monetary policy, which aims to manage inflation and unemployment. Key rate types used in this context include Nominal, Real, Negative, and Neutral.

Nominal Interest Rate

The Nominal Interest Rate is the official rate set by the central bank. It is adjusted using two primary approaches:

- Rate Cuts (Expansionary Policy): Reducing the rate lowers borrowing costs, boosting loan demand, supporting economic growth, and directing liquidity toward riskier markets.

- Rate Hikes (Contractionary Policy): Increasing the rate raises borrowing costs and the returns on low-risk assets, constraining credit growth, slowing economic activity, and curbing inflation.

Negative Interest Rate in Monetary Policy

- A Negative Interest Rate requires depositors to pay the bank to hold funds.

- This extreme form of ultra-easy monetary policy is implemented to combat deflation or recession by discouraging saving and encouraging immediate consumption and investment.

Real Interest Rate in Monetary Policy

- The Real Interest Rate is calculated by adjusting the nominal rate for inflation:

$$\text{Real Rate} = \text{Nominal Rate} - \text{Inflation}$$ - A Positive Real Rate acts as a contractionary policy, as borrowing costs exceed inflation.

- A Negative Real Rate acts as an expansionary policy, supporting borrowers and producers since the cost of debt is below the general price increase.

Neutral Interest Rate

- The Neutral Interest Rate is the level at which monetary policy is neither restrictive nor stimulative, allowing for steady economic growth.

- If the actual rate is above the neutral range, the policy is contractionary; if below, it is expansionary.

Impact of Interest Rates on Financial Markets

Interest Rate changes significantly influence liquidity and market sentiment, affecting various asset classes.

- Stocks and Cryptocurrency: These risk markets typically benefit from rate cuts (expansionary policy) due to increased liquidity and easier financing conditions for businesses. Conversely, they are negatively impacted by rate hikes (contractionary policy), which foster risk aversion.

- Gold: Gold prices usually rise gradually during rate-cut cycles as its value is inversely related to the dollar's strength and the yield on low-risk assets.

- Global Trade and Forex: Interest Rate differentials are a major factor in capital flows and exchange rate fluctuations. Higher rates attract foreign investors, strengthening the national currency, which makes exports more expensive but imports cheaper.

Conclusion

The Interest Rate is the fundamental cost of borrowing money and serves as the main tool of monetary policy. Its movements directly influence the entire financial landscape.

- Expansionary Policy (Rate Cuts): Increases liquidity, lowers borrowing costs, and generally benefits risk assets such as stocks and cryptocurrency.

- Contractionary Policy (Rate Hikes): Curbs economic growth, controls inflation, and typically leads to risk aversion in financial markets.

- Global Impact: Interest Rate differentials between countries drive international capital flows, significantly affecting exchange rates and global trade patterns.

Understanding the difference between simple and compound rates for investing, and recognizing the policy implications of nominal, real, and neutral rates, is crucial for navigating the financial markets.