Price growth edges lower despite reasonable economy

Insight

The RBA this afternoon and Powell interview in Washington tonight are today’s main draw cards.

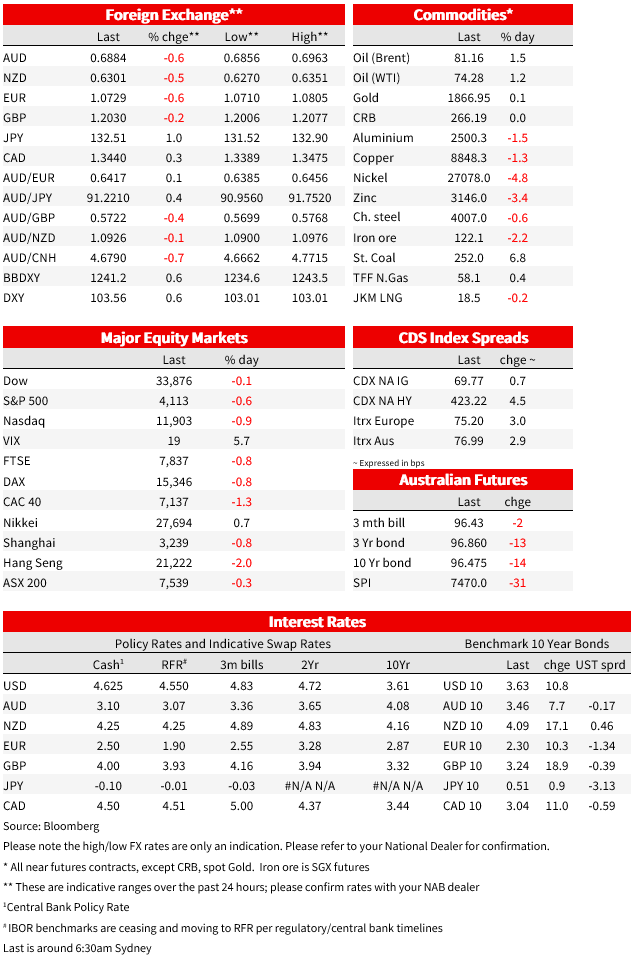

Friday’s violent market moves in the wake of both the eye-poppingly strong US employment report and sharp bounce in the Services ISM survey, have extended overnight. US Treasury yields are 15bps higher at 2-years and 10bps at 10-years, US stocks are entering the last hour of NYSE trade down about half a percent and the USD is 0.6-0.7% stronger in index terms. This has seen the AUD’s recovery back to the mid-0.69s during our time zone reversed, with a new low of 0.6856, reducing its year-to-date gains to a little less than 1% though still leaving it as the best performing G10 currency so far this year. The RBA this afternoon and Powell interview in Washington tonight are today’s main draw cards.

With nothing new out of the mouths of Fed officials to soothe market nerves after San Francisco Fed President Mary Daly on Friday described the surge in US non-farm payrolls as a ‘wow number’, bond and equity markets have been left to digest the likelihood that the Fed will now validate its own median 2023 ‘dot’ that sees the Fed taking the Funds Rate target range up to a peak of at least 5.00-5.25%, having refused to entertain a rate above 5% in the weeks leading up to Friday’s US data. The July FOMC date is now priced for a 5.123% Funds rate, i.e. the mid-point of a 5.0-5.25% target range. Money markets nevertheless continue to insist that rates will be coming down within 6 months of the peak being reached – consistent with historical averages but which may be a particularly poor guide in this unique pandemic and post pandemic era – with the January 2024 Fed meeting currently priced at 4.58%.

US equity markets aren’t being given quite the same treatment as bond or currencies, which makes sense in so far as risk markets are, for the time being at last, in a position to take back some of the recession risk premium (discount) given that January economic data couldn’t be telling a more different story regarding imminent recession (not that there has been much sign of them doing that in the first place seeing as how stocks have been off to the races since last October).

Bonds on the other hands are bearing the full brunt of revised Fed policy thinking, the 2-year note yield having now added 34 bps since Friday’s data releases and 10s 23bps (the irony being that this means that the yields curve recession signal has become stronger). So too are FX markets , currencies having to confront both the smartly higher US yield environment and the – for now – contradiction of the notion that the US economy has lost its global growth leadership role. That said, we’d note stronger than expected German December factory orders data last night (3.2% versus 2.0% expected with November revised up by more than 1%). More broadly, the likes of Citi’s economic surprises indices show that these have, collectively, been far more positive for both the EU and China in the last couple of months than the US, the latter even including last Friday’s numbers.

The only other data points of note overnight have been the EU Sentix investor sentiment index, which improved by more than expected to -8 from -17.5, and EU retail sales which were much in line with expectations -2.7% m/m (-2.5% expected but November was revised up to 1.2% from an original 0.8%).

Monday’s currency moves have brought the losses over the past two trading days to more than 2% for the SEK (2.3%) NZD (2.6%) AUD (2.6%) NOK 2.7%) and JPY (2.85%). The yen’s wooden spoon award reflects some independent weakness after the local press reports Sunday that currency BoJ deputy Governor Amamiya, considered a dove and the ‘continuity candidate’ when Mr Kuroda steps down in April, is the favoured successor. There have since been various official denials than Amamiya is the chosen one, not that anyone is minded to believe them.

While there have been no Fed speakers overnight, the BoE’s chief economist Huw Pill has been speaking, where he says that the chances of embedded inflation is higher in the UK than EU, but that while he’s not comfortable calling a turning point in rates, rate rises can probably now be less aggressive (a clear hint of +25bps – at least on his recommendation – next month). Pill reckons US rates may need to stay higher for longer but not in the EU. UK money market currently price Base Rate a shade above 4.25% against the current 4.0%.

For further FX, Interest rate and Commodities information visit com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.